.svg)

Financial security with an interest rate cap

You can now get a free interest rate cap for a new home loan for up to three years. The value of this benefit can be as much as 1,400 euros on a home loan of 150,000 euros.

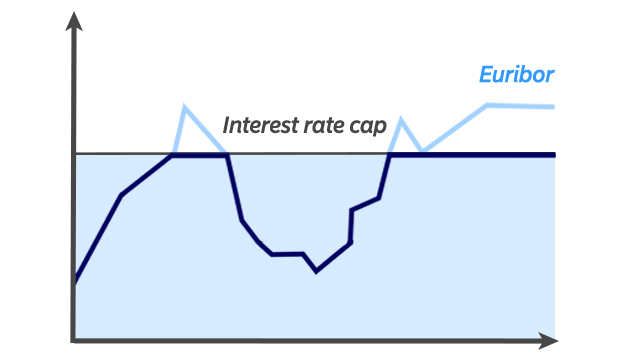

An interest rate cap prevents your monthly payment from exceeding a certain limit, adding stability to your finances. If your loan has an interest rate cap, you can focus on your new home without needless stress.

Benefits of an interest rate cap

- Protects your loan from a sharp rise in the reference rate. The interest rate will not exceed the agreed cap level even if the reference rate rises above it.

- On the other hand, you will benefit whenever the Euribor rate goes down – all the way to zero per cent.

- A loan with an interest rate cap is as flexible as any other home loan, and by using FlexiPayment, for example, you can increase or decrease your monthly payment without asking us first.

The free interest rate cap for a new home loan may have different features than other interest rate caps. This includes the validity period and cap level, for example. The loan period and repayment schedule can be agreed freely, but the loan period must be at least as long as the validity of the interest rate cap.

We will agree with you on a free interest rate cap during the loan negotiation, but the precise level and validity of the cap will be set when you draw down the loan. This interest rate cap is available for up to 3 years.

In this example, the value of the benefit is calculated using a home loan of 150,000 euros with an interest rate cap of 3.75% for three years, and the reference rate on the loan is the 12-month Euribor. The example is indicative and has been calculated using interest rate data from 25 March 2026. The value of the benefit varies depending on the amount of your home loan and the current level of the interest rate cap.