.svg)

Earnings growth supports the outlook

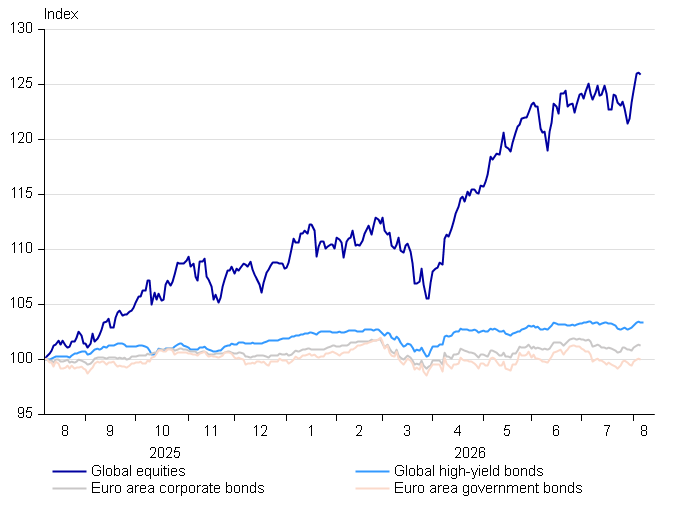

The optimism surrounding peace in the Middle East at the end of June quickly faded as the crisis escalated once again in early July. Rising oil prices and concerns about the sustainability of AI investments caused some jitters in both the fixed income and equity markets. However, a more significant decline was largely confined to the semiconductor sector, driven in part by the unwinding of speculative investments. Strong earnings growth continues to support the equity market outlook, and we therefore recommend maintaining an overweight position in equities.

AI boom faces a reality check

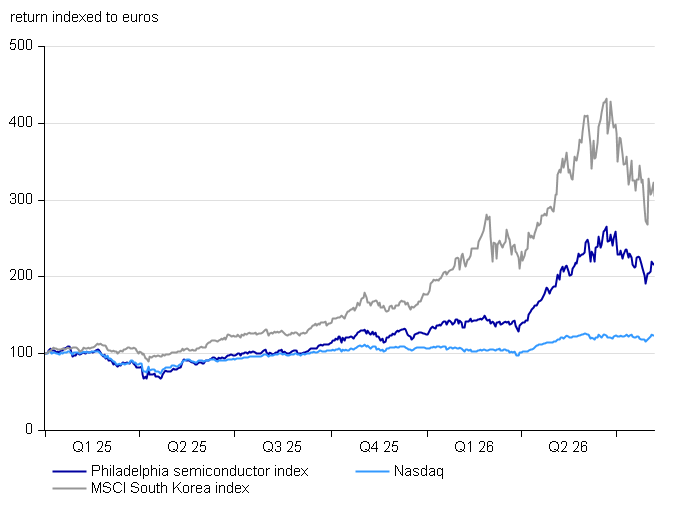

Massive investments in high-performance data centres have particularly benefited semiconductor companies that design and manufacture processors, memory chips and other components used to train and run AI models. Revenues in the sector are expected to nearly double this year, driven by both rising volumes and higher sales prices. In the second quarter, South Korean chip manufacturer Samsung made history by reporting an operating profit of USD 62 billion, setting a new global record for quarterly earnings. The previous record, held by Nvidia, stood at “just” USD 53.5 billion.

The semiconductor sector has been a favourite among investors in 2026, delivering very strong returns during the first half of the year. Following a peak around Midsummer, however, the sector experienced a correction of around 20% after announcements of capacity expansions raised concerns about weaker profitability. The steepest decline in share prices, approaching 40%, occurred in South Korea, where local retail investors had gained leveraged exposure in Samsung and SK Hynix through ETFs. Such instruments can generate attractive short-term gains during a rising market, but they can just as easily lead to sleepless nights when markets move lower.

AI investment has grown to such an extent that even the largest companies can no longer finance it entirely through their cash flows. Microsoft, Meta, Amazon and Alphabet alone are expected to invest a combined USD 750 billion in AI this year, representing a 70% increase from last year. As much as half of these investments will be financed through the bond market. Next year, investment by these hyperscalers is expected to reach USD 1 trillion, increasing their need for external financing. So far, raising capital has not posed any difficulties, with investors consistently oversubscribing their bond issues. More recently, however, demand has been somewhat less robust than in previous issues, and investors are expecting higher yields. It is therefore important for the hyperscalers to convince investors of the profitability of their investments in order to keep financing costs under control. Encouragingly, the messages regarding demand delivered during the summer earnings season were broadly positive, particularly among companies providing cloud services.

Tensions in the Middle East remain elevated

At the end of June, Iran and the US signed a memorandum of understanding intended to restore normal traffic through the Strait of Hormuz without delay. Oil prices fell sharply in June, prompting expectations that the oil market could face an oversupply situation later in the year. However, that optimism proved premature. The conflict escalated again in July, sending oil prices higher once more. According to the latest reports, negotiations are continuing and US officials have indicated that an agreement may be within reach. That said, investors have heard similar assurances on several occasions before.

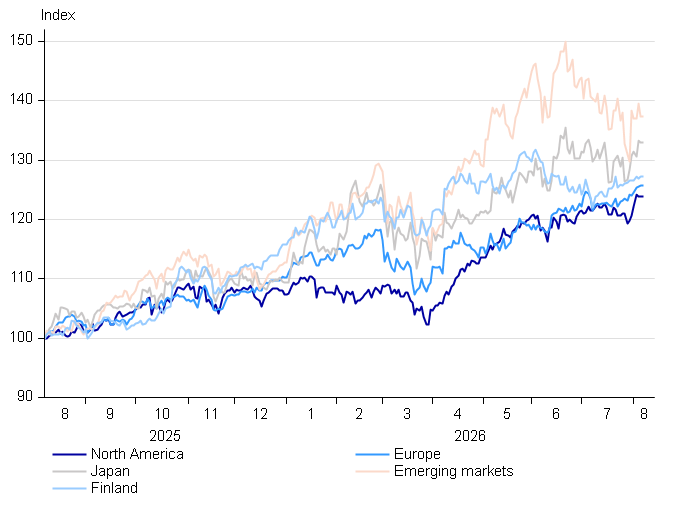

On the bright side, the global economy has so far shown considerable resilience in the face of the conflict. Economic growth in the US has remained strong, supported by robust consumer demand and continued investment activity. Even in Europe, where economies are more dependent on imported energy, growth in the second quarter was clearly stronger than expected. Europe’s industry has continued to recover, while confidence in the service sector has rebounded from the downturn that followed the outbreak of the Iran conflict. Even Finland’s economy has delivered relatively strong growth, supported by solid export performance and early signs of a recovery in consumer spending.

Earnings growth remains exceptionally strong

The second-quarter earnings season has been significantly stronger than expected in both the US and Europe. Earnings growth is on track to exceed 20% in both regions, more than double the pace typically seen. Most importantly, earnings growth has been relatively broad-based rather than driven solely by tech companies. Energy and materials companies have benefited from strong commodity prices, while banks and industrial companies have also reported robust earnings growth.

Tighter monetary policy expected

Higher oil prices have added to inflationary pressures, although stronger demand has also contributed to rising prices. The European Central Bank (ECB) raised its policy rate in June but left it unchanged at its July meeting. However, the ECB has signalled that it will continue to hike rates, and markets are currently pricing in the next rate hike for September.

The US Federal Reserve also kept its policy rate unchanged in July, but the decision was not unanimous, with three members of the Federal Open Market Committee voting in favour of a rate hike. This suggests that the Fed’s next move is more likely to be a hike, although the timing remains uncertain. The Fed’s leadership changed in May, and the new Chair, Kevin Warsh, has adopted a notably more reserved communication style. The era of clear forward guidance therefore appears to be behind us. For now, market expectations point to the next rate hike taking place in December.